Impact of Hurricane Ernesto on Property Claims

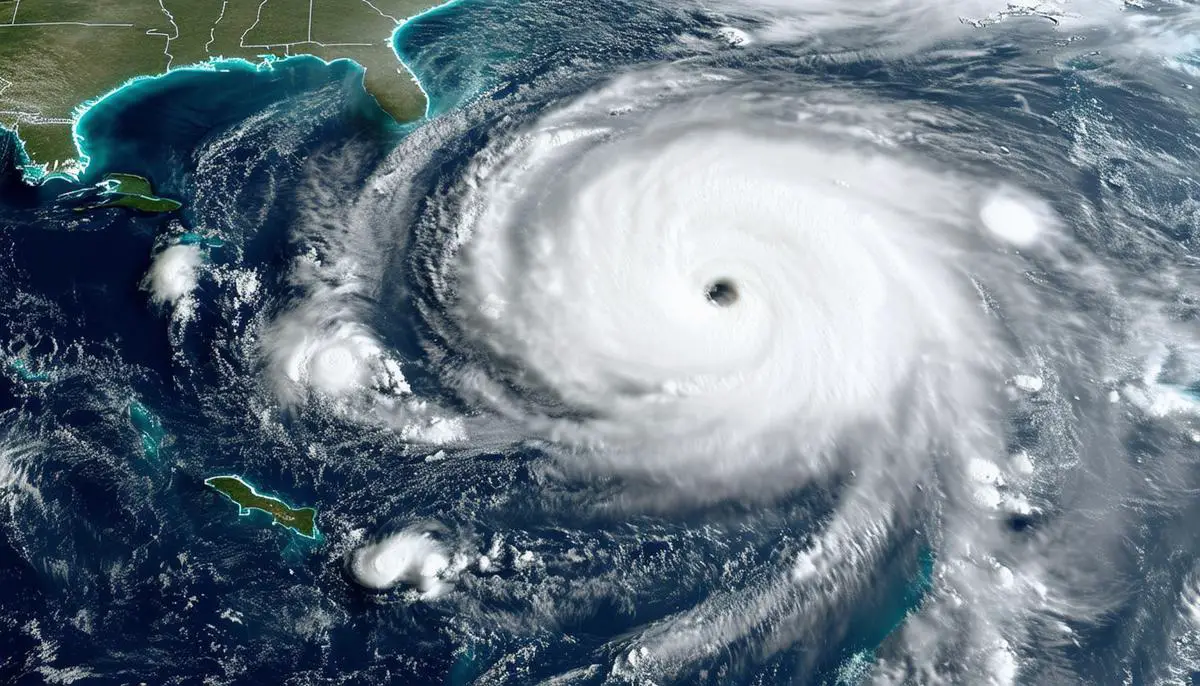

Hurricane Ernesto made landfall in Bermuda as a Category 1 hurricane, bringing maximum sustained winds of 85 mph and gusts reaching 84 mph. Bermuda's stringent building codes helped minimize structural damage, with limestone and concrete block buildings withstanding the winds well. Some power outages occurred but were promptly restored.

Storm surge and heavy rainfall were notable aspects of Ernesto:

- Tidal gauges around St. George Island showed surge tides peaking 1 to 2 feet above Mean High High Water

- 5.4 inches of rain fell on Aug. 16

- Low-lying coastal areas faced significant flooding

Insurers estimate insurable losses to remain minimal, thanks to Bermuda's construction standards and preparedness.

In Puerto Rico, the impact was more severe. Initially a tropical storm, Ernesto brought substantial rains and winds to the island. Puerto Rico's agricultural sector reported losses of $23.5 million, with plantains, coffee, and vegetables taking the hardest hits. Around $1.2 million was reported in forage losses, and hydroponic structures also faced considerable damage.

Despite the challenges, initial feedback from AM Best-rated companies indicates that property losses will likely remain moderate. Much of the damage stemmed from storm surge and flooding, the latter not typically covered under standard homeowners' policies. Insurers pointed out that many policyholders did not have power outage endorsements, which could complicate business interruption claims.

Insurers have been proactive in reaching out to policyholders. Farmers with insurance through the Agricultural Insurance Corp. (CSA) have been urged to file claims, while additional assistance is available from the USDA's Federal Farm Service Agency. Efforts to aid uninsured farmers ineligible for CSA support are also underway.

The claims process may prove challenging given Puerto Rico's infrastructure issues. Widespread power outages and transportation problems complicate efforts further. Even with these hurdles, the initial damage estimates suggest that the financial impact on insurers will be manageable, staying within reinsurance coverage limits.

Reinsurance's Role in Managing Losses

Reinsurance played a critical role in Puerto Rico's ability to absorb and manage property losses from Hurricane Ernesto. The storm surge and flooding caused moderate damage, but the effective use of reinsurance agreements ensured that insurers could handle claims without significant financial strain.

Since the devastating impacts of Hurricanes Maria and Irma in 2017, Puerto Rican insurers have strategically increased their reliance on reinsurance. From 2018 to 2023, the percentage of premiums ceded to reinsurance companies has more than doubled. In 2023, unaffiliated Puerto Rico-domiciled companies held a 78% share of total net premiums written (NPW), up significantly from 68% in 2018.

This increased reliance on reinsurance has provided a strong buffer against catastrophic losses. By transferring a larger portion of risk to reinsurance firms, local insurers have been able to maintain healthier balance sheets and better navigate the financial fallout from severe weather events.

"The aftermath of Hurricane Ernesto highlighted the importance of these reinsurance strategies. While the storm caused significant damage, the insured losses remained comfortably within the limits of reinsurance coverage."

Discussions with AM Best-rated companies revealed that property losses were on the lower side of the modelled projections, thanks to the extensive reinsurance agreements in place.

Puerto Rican insurers have also benefitted from improved capital positions due to favorable operating profitability in recent years. Since the declines observed in 2017 and 2018, aggregated capital and surplus for these companies have reached ten-year highs. This improved financial health has bolstered their ability to withstand losses and reflects a broader trend of increased preparedness and resilience within the insurance sector.

The strategic use of reinsurance has allowed insurers to manage their current claims and provided a foundation for quicker recovery and continued market stability. As the claims process unfolds, the presence of reinsurance support ensures that even smaller insurers can manage losses effectively without substantial impacts on their capital positions.

Business Interruption and Infrastructure Challenges

Hurricane Ernesto presented significant challenges in terms of business interruptions and infrastructure degradation. Widespread power outages created a ripple effect that hampered recovery efforts and the overall claims process. For businesses, particularly those without comprehensive commercial policies, the storm underscored the critical importance of having specific endorsements to cover power outages.

Jason Hopper, an associate director at AM Best, highlighted the unpredictability of business interruption losses during this period. Many businesses that included commercial policies often overlooked power outage endorsements, leaving numerous enterprises vulnerable to prolonged downtimes and operational disruptions.

Infrastructure Challenges:

- Widespread power outages across Puerto Rico

- Weakened supply chain facing delays

- Roads and bridges damaged or obstructed by debris

- Delayed assessments and repairs

These physical infrastructure issues further compounded business interruptions. The island's weakened supply chain faced delays, with essential supplies for rebuilding and repairs taking longer to reach affected areas.

Insurers responded by advising policyholders to review and update their commercial policies to include comprehensive endorsements that cover potential interruptions such as power outages. They emphasized the necessity of forward planning and risk management strategies to mitigate the financial impacts of natural disasters.

The aftermath of Ernesto illustrated a lesson in preparedness and adaptability. Insurers noted the increasing need to educate policyholders on the benefit of expanded coverage options. Comprehensive plans that include endorsements for power outage, supply chain interruptions, and other infrastructure-related disruptions are now essential components of risk management in disaster-prone areas.

Economic and Agricultural Sector Impact

Hurricane Ernesto's impact was notably felt in Puerto Rico's agricultural sector, causing considerable damage with reported losses of approximately $23.5 million. The breakdown of losses is as follows:

| Crop/Area | Loss Amount |

|---|---|

| Plantains | $11.5 million |

| Coffee | $2.5 million |

| Vegetables | $2 million |

| Bananas | $1 million |

| Forage | $1.2 million |

| Hydroponic systems | $1 million |

| Infrastructure (roads and farm preparations) | $2 million |

| Citrus and fruit sectors | $800,000 |

To address these economic challenges, the government and insurance providers have taken several measures to support the recovery of the agricultural sector. Agriculture Secretary Ramón González has emphasized the importance of the agricultural sector to Puerto Rico's economy and assured that comprehensive efforts are in place for its recovery.

Support measures include:

- Farmers insured through the Agricultural Insurance Corp. (CSA) advised to initiate claims promptly

- Support from the USDA's Federal Farm Service Agency (FSA) and the Noninsured Crop Disaster Assistance Program (NAP)

- Coordination between farmers and the Agricultural Enterprise Development Administration (ADEA)

- Regional agronomists conducting farm visits to assess losses and guide farmers in the claims process

- Encouragement for insured farmers ineligible for CSA coverage to file new claims through regional offices

The measures taken by both government entities and insurers reflect a coordinated response aimed at addressing immediate needs and rebuilding the agricultural infrastructure. This proactive stance is critical for sustaining the agricultural economy in the aftermath of such natural disasters.

In conclusion, the resilience and preparedness demonstrated in the face of Hurricane Ernesto highlight the importance of strong infrastructure and strategic reinsurance. The proactive measures taken by insurers and government entities have played a crucial role in managing losses and ensuring a swift recovery for affected communities.

- González R. Agricultural Sector Recovery Plan Following Hurricane Ernesto. Puerto Rico Department of Agriculture. 2023.

- Hopper J. Business Interruption Claims in the Wake of Natural Disasters. AM Best. 2023.

- Puerto Rico Insurance Commissioner's Office. Reinsurance Trends in Puerto Rico: 2018-2023. Annual Report. 2023.

- National Hurricane Center. Hurricane Ernesto: Meteorological Report. 2023.

- USDA Federal Farm Service Agency. Disaster Assistance Programs for Agricultural Producers. 2023.

![]()